Money management.

They don’t exactly teach it in high school or college. Many of us are left to “figure it out” and some of us are better at figuring it out than others.

To boot, there are lots of opinions floating around on how to manage your money successfully, but sifting through all that can be paralyzing.

We’ve got you covered though. Here are our 7 top recommendations for managing your finances:

1. Do: Plan Your Spending Before the Money Arrives

You are the CEO and CFO of You, Inc. Think about running your personal finances like a business. Companies plan their revenues and expenses well in advance. Budgeting gets a bad rep, but successful, profitable businesses formally plan their finances and make spending decisions in advance.

Money is like a toddler. If you don’t monitor it carefully, it will wander off and disappear quickly! Click To Tweet

We all saw what happened in Cincinnati. Don’t let that happen to your money.

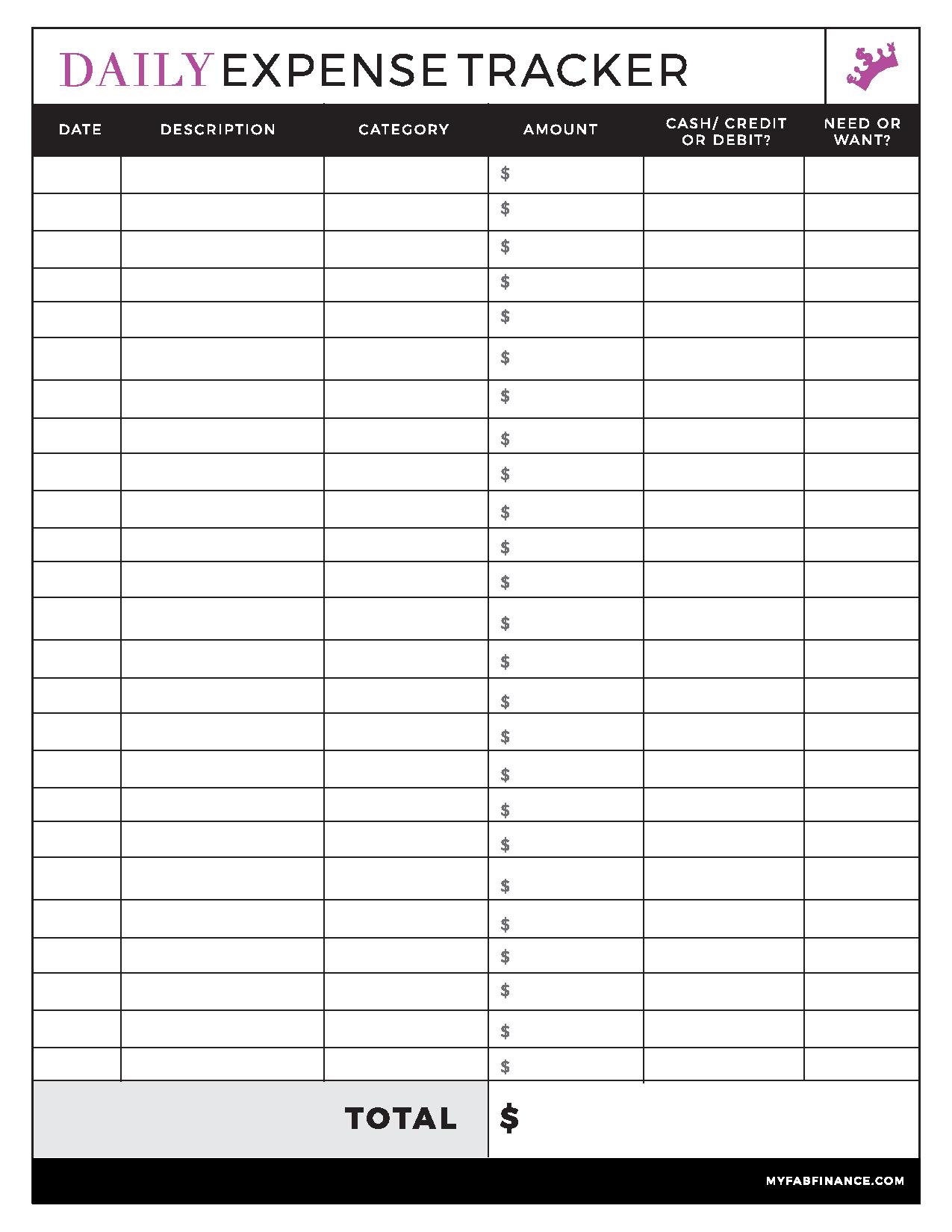

2. Do: Aggregate Your Accounts and Track Your Spending

Aggregating your accounts allows you to see the big picture and your net worth, a number we highly recommend you track regularly. It can be even more difficult to make tough choices if you don’t have the bigger picture in mind. Expense tracking is also important.

Grab the My Fab Finance expense tracker here:

You cannot change what you do not measure. Click To Tweet

In order to make meaningful change, know exactly how much you spent last month versus the month prior. Guessing doesn’t work well with personal finances. Once you build a habit of tracking your finances, making smart money decisions becomes much easier.

3. Do: Understand and Deal with Your Impulse Purchases

Impulses. For some it’s the mall, for others it may be online shopping. Have you ever gone into a store planning to spend $50 and but end up spending $300? It is a marketer’s job to turn a “want” into a “need.” Have you ever noticed that television commercials usually do not reveal the product or company until the end of the commercial? . Instead of selling a can of soda, they are selling happiness, desirability or beauty. Instead of a gym shoe, peak athletic performance is sold. Instead of selling their own product, the product or company receives a celebrity endorsement. Companies hire social scientists who study human behavior, emotions and decision-making to gain a marketing edge.

Here are some ways to protect yourself and your wallet:

- 24-hour rule – Wait at least 24 hours before making purchases over a certain amount

- Do not buy items you didn’t leave the house for

- Deconstruct advertisements: what are they really selling?

- Use cash for non-regular expenses

- Don’t fall for your own excuses (“I deserve it”, “it’s on sale”, “I’ll pay it off next month”)

4. Do: Develop a Habit of Saving and Automate It.

Even if you start small (i.e. $25/week), put systems in place that force you to save. The government understands this very well, which is why employee payroll taxes come out of your paycheck even before you are able to touch it. Apply the same strategy for your savings. Some employers will allow splitting your paycheck to different bank accounts (i.e. 75% checking, 25% savings). Another idea is to set a recurring transfer from your checking account to your savings on the same schedule as your paycheck.

There are other automatic features to consider such as:

- Auto escalating your 401k contributions – some employers with a 401(k) offer an option to automatically increase your retirement savings by a certain percentage on a regular basis (i.e. increase 1% annually)

- Keep the change features in checking accounts – Some checking accounts will round up your purchases and put the change in your savings account. It is the e-version of the piggy bank. If you purchase an item for $5.60, it will round up to $6.00 and $0.40 will be deposited in your linked savings account.

- Sign up for Digit, a web app that automatically saves money for you.

5. Don’t: Ignore Your Credit Score and Credit Report

Your credit score is important. It is your adult GPA. While it isn’t everything, you will eventually need it. Credit scores have traditionally been used to evaluate creditworthiness for extending loans (e.g. personal loans, mortgage, car loans, credit cards). Typically you appear more creditworthy with a higher credit score. The reality is that both credit scores and credit reports are being used beyond financial transactions. Credit scores and reports are used by prospective employers, landlords/homeowners, insurance companies, and even utility companies such as cell phones and cable providers. The challenge is credit reports often have mistakes which can negatively impact your credit.

Check out our resources on checking both your credit report and credit score.

6. Don’t: Ignore Your Workplace Benefits

If you work for a company and do not understand the full scope of your employee benefits, it may be time to check out your HR Benefits website or schedule a meeting with a representative from the HR office. There are often benefits that go underutilized that can save you hundreds if not thousands annually.

One of the most beneficial employer benefits is the 401k/403b match. For most people this is a no-brainer, you are essentially rewarded for putting money aside for your future. Wellness initiatives can often mean big savings as well. Many companies are offering rebates on health insurance premiums for wellness activities, such as physicals or wearing fitness trackers. Let’s think about that for a second, companies are paying additional cash to employees to be healthier.

There are several other types of benefits, such as commuter benefits, disability insurance, life insurance, child care benefits, education benefits, product discounts and even student loan repayment programs. Make sure you maximize the benefits that are offered to you.

7. Don’t: Keep up With the Joneses

Most people are familiar with the term “Keeping up with the Joneses,” which refers to making material purchases based upon your social circle. The idea is that if your neighbors or friends buy a new car, you should too. We call this the comparison trap and it’s one of the lessons we learned paying off our student loan debt.

Part of the problem with comparing your financial status with others is that it is very difficult to know someone’s complete financial picture. Money is still a private topic and everyone has different income, expenses, debt obligations and assets. The people you are comparing yourself to could be completely up to their eyeballs in debt or fund their lifestyle through an inheritance. Making comparisons, not only could be comparing apples and oranges, but it also casts your own possessions in a negative light.

“Comparison is the thief of joy” – Mark Twain Click To Tweet

A few reasons why keeping up with the Joneses is a bad idea:

- News Alert! The Joneses are broke! According to a recent Bankrate survey, 76% of Americans are living paycheck to paycheck with little to no emergency savings. Why keep pace with people that are one emergency away from financial catastrophe?

- When you compare yourself to others, it’s much easier for wants to become needs. Wanting a car becomes needing a brand new SUV. Technology like smart phones, that didn’t exist 10 years ago, are a now a necessity. We have a desire to show off and have our success validated by others.

- Companies are spending billions of dollars to market their products and services to you. Many luxury brands are selling a temporary feeling of exclusivity in exchange for premium pricing. It is easy to get sucked into the culture of consumerism. Happiness from possessions is always temporary and fleeting.

Let’s face it. We live in a culture with an economy fueled by consumer spending. These recommendations will enable you to keep more of your income to reach your financial goals.

You said: